Why the rules are broken, the mistakes are invisible, and your portfolio may already be living in the past

First, Let’s Get the Basics Right

Before we talk about what’s broken, it helps to be clear on what asset allocation actually means because the term gets used loosely, often interchangeably with “diversification” or “portfolio planning,” and they are not the same thing.

Asset allocation is the deliberate decision of how to divide your wealth across different asset classes such as equity, debt, real estate, gold, cash, and alternatives, with the goal of balancing growth, risk, and liquidity in a way that is specific to your life and your financial goals.

It is not a one-time exercise. It is not a fixed percentage. And it is not the same for everyone.

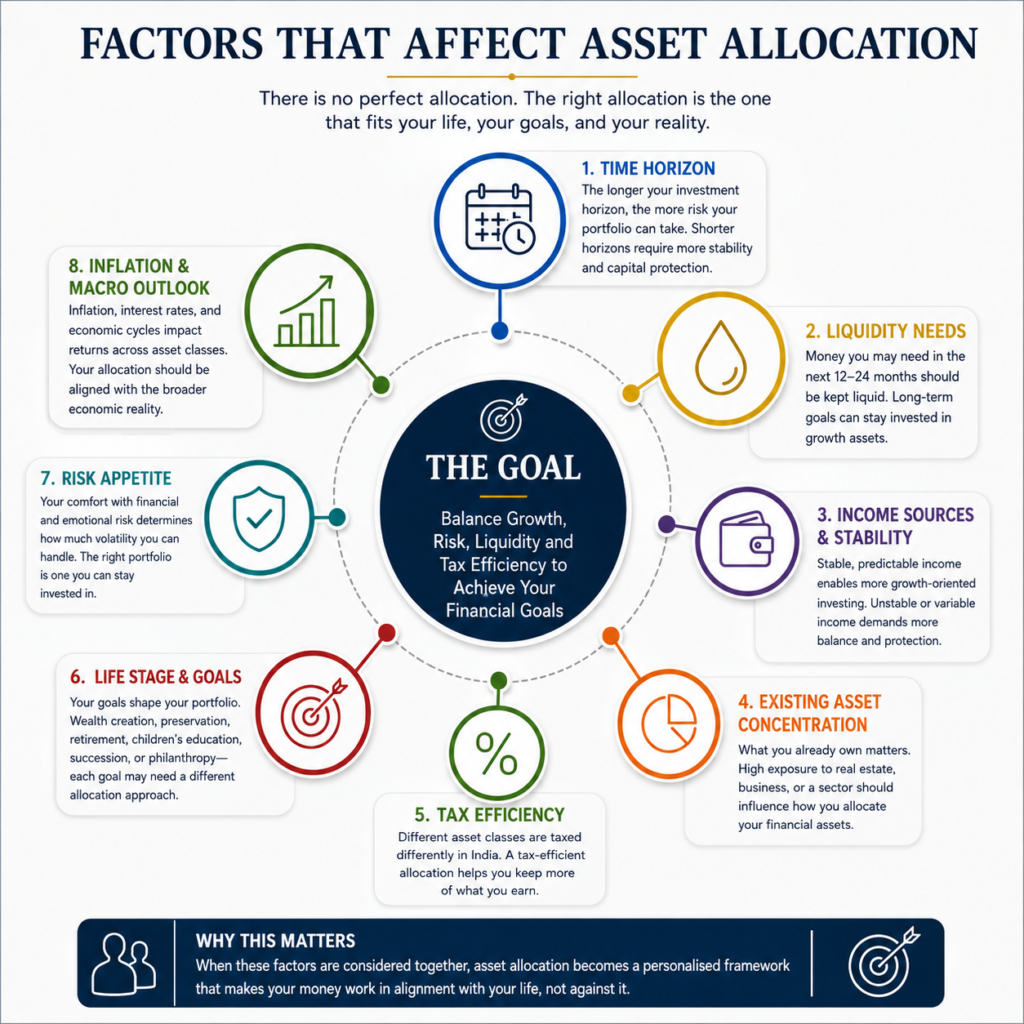

The right allocation for any individual depends on a combination of factors that are deeply personal:

Time Horizon

A 38-year-old business owner building generational wealth has a fundamentally different investment runway than a 60-year-old planning for retirement income. Longer horizons allow for higher equity exposure and more tolerance for short-term volatility.

Risk Appetite

This is both financial and psychological. Can your portfolio absorb a 30 percent drawdown without forcing you to sell? And more importantly, can you? These two questions have different answers for different people, and both matter.

Liquidity Needs

How much capital do you need accessible within the next 12 to 24 months? Business obligations, family expenses, and planned acquisitions all shape how much of your portfolio should remain liquid versus locked into long-duration assets.

Income Sources and Stability

An investor with predictable, recurring income can afford to be more aggressive in their portfolio. Someone whose wealth is tied to a cyclical business needs more stability as a counterbalance.

Existing Asset Concentration

Most Indian HNI families hold a significant portion of their net worth in real estate or a family business. This pre-existing concentration must be factored into any allocation decision. Otherwise, you are diversifying on paper while remaining concentrated in reality.

Tax Efficiency

Different asset classes carry different tax treatment in India. A well-constructed allocation is not just about returns. It is about what you actually keep after taxes.

Life Stage and Goals

Wealth accumulation, wealth preservation, business succession, children’s education, and philanthropy all influence how wealth should be structured.

When all of these factors are genuinely accounted for, asset allocation becomes something powerful: a customised framework that makes your money work in alignment with your life, not against it.

The problem is that most investors, including very sophisticated ones, do not actually allocate this way. Instead, they follow borrowed frameworks, make individually smart decisions that do not add up to a coherent whole, and build portfolios designed for a world that no longer exists.

Let’s dive into each problem individually.

If you have spent any time in wealth management circles, you have heard some version of the same advice: diversify your portfolio, follow a structured allocation, and rebalance periodically.

It sounds sensible. It is sensible, in theory. But here is what that advice rarely tells you: the framework most Indians use to allocate their wealth was borrowed from a different country, built for a different era, and is quietly failing a different kind of investor. This blog is about all three of those hidden asset allocation risks.

The Three Hidden Layers of Asset Allocation Risk

| Layer of Risk | What It Looks Like | Why It Matters |

| Structural Risk | Following outdated frameworks like the traditional 60/40 model | The framework may not suit Indian markets or Indian HNI balance sheets |

| Hidden Concentration Risk | Owning multiple investments exposed to the same underlying economic risks | Portfolios appear diversified but fall together during stress |

| Outdated Assumption Risk | Keeping allocations unchanged despite changing market realities | A portfolio built for yesterday’s environment may no longer fit today’s world |

Part One: The Rule That Was Never Really Yours

Let’s start with the 60/40 rule because it is the foundation most allocation conversations are built on. Sixty percent in equities for growth. Forty percent in debt for stability.

It is taught in finance courses, repeated by advisors, and followed by millions of investors across the world.

What almost no one mentions is where it actually came from. The 60/40 framework was designed in post-war America for a market defined by deep, liquid bond markets and a reliable negative correlation between stocks and bonds. When equities fell, bonds rose and cushioned the blow. That dynamic worked elegantly for decades.

Then 2022 happened.

Equities fell sharply and bonds fell with them. The foundational assumption of the entire framework weakened in real time, in full view, and the financial world largely moved on without seriously rethinking the model.

The numbers tell the story clearly: 2022 was the only year in the last four decades when stocks and bonds both posted significantly negative returns at the same time. U.S. equities dropped approximately 19 percent while the broad bond index fell around 13 percent, marking the worst joint performance for the pair in over 40 years. A typical 60/40 portfolio declined roughly 16 to 17 percent that year, its worst single-year performance since 1937. [1, 2]

In India, that assumption was always less reliable than many admitted. Indian debt instruments do not consistently rally when equities correct. They often continue earning modest returns while inflation quietly erodes real purchasing power. India’s long-term retail inflation has typically remained around 5 to 6 percent. Many traditional debt instruments, especially after tax, barely keep pace with that reality.

To put this in context: according to government data, India’s average retail CPI inflation over the ten-year period from 2015-16 to 2024-25 was approximately 5 percent per annum. A fixed deposit returning 6 to 6.5 percent pre-tax translates to roughly 4.5 to 5 percent post-tax for investors in the 30 percent bracket, leaving little to no real return after inflation. [3]

But the deeper problem is not even the debt side. It is what the framework ignores entirely.

Most Indian HNI families already hold 60 to 70 percent of their net worth in real estate through ancestral properties, commercial assets, or residential holdings accumulated over generations. Their financial portfolio may appear balanced on paper. Their actual wealth picture is often heavily concentrated in one illiquid asset class.

According to Knight Frank’s Wealth Report 2024, approximately 32 percent of India’s HNIs allocate a significant share of their wealth to residential real estate alone, and the average Indian HNI owns 2.57 homes. This is before accounting for commercial holdings or business-related real estate. [4]

Adding another large allocation to low-yield debt on top of an already real-estate-heavy balance sheet is not necessarily conservative investing. In many cases, it is compounding the same concentration twice and calling it diversification.

And then there are the asset classes the traditional framework barely accommodates at all: Sovereign Gold Bonds, REITs, InvITs, AIFs, unlisted equity, and pre-IPO opportunities. India’s investment landscape has evolved enormously. A two-asset-class framework designed for another market in another decade simply cannot fully capture that complexity anymore.

Part Two: The Mistake That Hides in Plain Sight

There is a particular type of investor who concerns us most. Not the beginner who knows little about investing. Not the retiree who keeps everything in fixed deposits. The investor we worry about is the one who has done almost everything right. They built a successful business, accumulated meaningful wealth and now work with a CA and an advisor and review the portfolio regularly. Despite being sophisticated and engaged, they are quietly making the same mistake many high-net-worth families make.

That mistake is optimising individual investments instead of the portfolio as a whole.

Here is how it usually happens.

An investor buys a commercial property because the rental yield looks attractive. They invest in a PMS because the manager has a strong five-year track record. They maintain a significant stake in their own business because they understand it deeply. They hold large fixed deposits “just in case.”

Individually, each decision appears reasonable. Sometimes even smart. But viewed together, a very different picture emerges. The commercial property, the business equity, the PMS with its sectoral exposure, and even the FD are often tied to the same underlying driver: the health of the Indian economy and, in many cases, a single industry cycle.

When conditions are favourable, everything rises together and it feels like intelligent planning. But when conditions deteriorate, everything falls together and there is nowhere to hide. This is concentration risk disguised as diversification. And it is one of the most common asset allocation failures among sophisticated investors.

Ironically, this mistake becomes more common as wealth increases. Familiarity breeds confidence. Investors naturally allocate heavily toward industries, cities, and businesses they understand personally.

Each investment may come through a different relationship and at a different time:

- the CA recommended the property,

- the banker introduced the PMS,

- the FD became a long-standing family habit.

Because the decisions are made separately, few investors step back and evaluate whether they actually make sense together.

True diversification is not about owning many things. It is about owning assets that behave differently from each other, especially during periods of stress.

The real test is simple:

If Indian growth slows sharply, credit tightens, and equity markets correct significantly, which parts of your portfolio decline together? How much of your wealth is exposed to that single scenario? And where is the genuine non-correlation?

Part Three: A Portfolio Built for Yesterday

Even if you began with a sensible framework and avoided concentration risk, another problem remains. The portfolio you built two or three years ago may have been designed for a world that no longer exists.

Cast your mind back to 2021-22. The investment environment looked a certain way:

- Interest rates were near historic lows globally, making debt unattractive and equities the obvious choice

- Indian small and mid-caps were in a multi-year bull run, and momentum strategies were winning

- Real estate was still recovering post-COVID, and most advisors were underweighting it

- Inflation seemed transitory, and most portfolios reflected that assumption

- Global diversification was an afterthought for most Indian HNI portfolios

If your allocation was last seriously reviewed in that environment, it was built on assumptions that may no longer hold true today. The interest-rate environment changed meaningfully. Debt instruments that once offered weak real returns now provide attractive yields in several categories.

A portfolio that intentionally underweighted debt in 2021 may remain underweight today simply because nobody revisited the original reasoning. Mid and small-cap valuations that looked compelling in 2020 are now considerably richer. The same funds that delivered extraordinary returns are now priced for far more optimistic expectations.

The valuation shift has been significant. At the market peak in September 2024, the Nifty Midcap 100 was trading at a PE of 45x and the Nifty Smallcap 100 at 36x, well above their long-term averages. Even after the correction that followed, the Nifty Midcap 100 still trades at a 26 to 30 percent premium over its historical average PE of 22.5x. Portfolios built on the return expectations of 2020-21 have not priced in this valuation reality. [5, 6]

REITs and InvITs have emerged as credible yield-generating and inflation-sensitive assets. Global diversification has become increasingly relevant as currency and geopolitical risks have become more pronounced.

None of these changes is catastrophic individually. But together, they create a quiet misalignment between yesterday’s allocation and today’s reality.

Most investors address this through mechanical rebalancing. If equity exposure rises from 60 percent to 70 percent, they trim it back. That approach is better than nothing. But mechanical rebalancing only preserves the structure of the original portfolio. It does not question whether the original structure still deserves to exist. Those are very different conversations. Only one of them is strategic.

What Good Asset Allocation Actually Looks Like

Having explored what is broken, it is equally important to define what better looks like. Good asset allocation for an Indian HNI investor today does not begin with a formula. It begins with honest questions.

What is my real exposure across everything? Not just financial assets, but real estate, business equity, receivables, and the family’s primary income source. Before reallocating capital, where is the actual concentration already sitting?

What happens during a genuine stress scenario? If Indian growth slows meaningfully, which parts of the portfolio decline together? How much of total net worth is exposed to the same economic outcome?

Where is the true non-correlation? Gold, select global equity strategies, and certain alternative assets often behave differently from Indian equity cycles. How much of the portfolio is genuinely independent of the same domestic growth story?

What are my actual liquidity needs? Not a generic emergency buffer, but a realistic assessment of capital requirements over the next 12 to 24 months. Debt allocation should reflect this reality, not a textbook percentage.

Is my portfolio built for the next decade or the last one? India’s future growth may increasingly be driven by infrastructure, manufacturing, domestic consumption, and a deeper capital market ecosystem. Is the portfolio positioned for those realities or for themes that have already played out?

These questions do not have universal answers.

A business owner in their forties with concentrated unlisted equity requires a very different allocation than a retired professional with inherited wealth and no active income. The point is not the formula, it is the thinking which matters.

The Real Cost of Getting This Wrong

Asset allocation is different from most financial decisions because the cost of getting it wrong often remains invisible until it suddenly is not.

A poor stock pick becomes obvious quickly. A bad insurance product eventually reveals itself. But a poorly allocated portfolio can appear perfectly healthy for years while quietly accumulating concentrated and correlated risk beneath the surface.

The investors who preserve wealth across generations are rarely the ones chasing the best-performing asset class. They are the ones who understand how every part of their wealth behaves together before the market forces them to.

The traditional 60/40 framework was never truly built for India. The mistake of optimising investments individually instead of collectively remains widespread. And the portfolio that worked well three years ago may already be misaligned with the environment ahead.

All three of these problems are fixable. But fixing them requires a different kind of conversation. One that begins not with which fund to buy next, but with an honest understanding of where your wealth actually sits today and how it behaves under pressure.

Asset allocation is not a one-time decision. It is an ongoing answer to a question that keeps changing. The real question is whether your portfolio is evolving with your life and the world around it, or whether it is still operating on assumptions that expired years ago.

References

[1] Morgan Stanley Investment Management, “The Big Picture: Return of the 60/40” (2023). Available at: morganstanley.com

[2] CAIA Association, “The 60/40’s Annus Horribilis” (February 2023). Available at: caia.org

[3] Press Information Bureau, Government of India, “Retail Inflation Hits Six-Year Low” (2025). Average CPI inflation of approximately 5 percent per annum over 2015-16 to 2024-25. Available at: pib.gov.in

[4] Knight Frank, “The Wealth Report 2024.” Key finding: 32 percent of Indian HNIs allocate significantly to residential real estate; average Indian HNI owns 2.57 homes. Available at: knightfrank.com

[5] Upstox Market Analysis, “Index Breadth Analysis: Nifty Midcap 100 and Nifty Smallcap 100 Valuations” (January 2025). Available at: upstox.com

[6] Finomics Edge, “The Indian Market Valuation Puzzle” (January 2026). Available at: medium.com